How to Read Your Insurance Claim

If you’re filing your first roof insurance claim, you may be confused by your claim summary. At Restoration Roofing, we get a lot of questions from customers on their insurance paperwork. To clarify, we are going to share an example of an insurance claim summary and break down each line item.

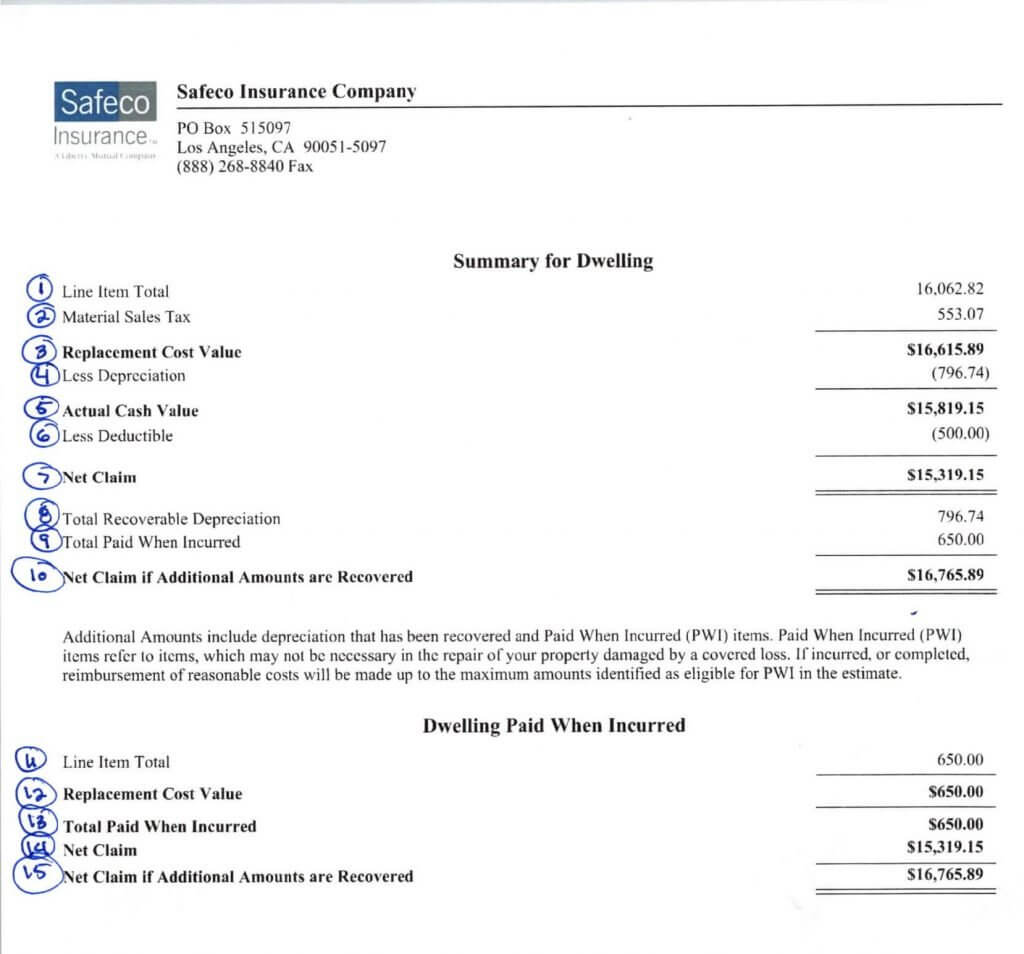

Claim Summary

A claim summary is an insurance adjuster’s estimate of the expected cost to repair or replace the damages on your roof.

Line Item 1: This is your line item total for materials and labor. This is the total of all the line items in the previous pages added up before tax.

Line Item 2: Line number two is the material sales tax. That’s where they’re adding your sales tax for your municipality in your state.

Line Item 3: Number three is the important number that we want you to pay close attention to. It’s usually in bold and it’s usually the biggest number on this list. That number is the replacement cost value. To summarize, replacement cost value is the value or what it costs to rebuild your roof back to a pre-loss condition and fix the whole roof.

Unless you have a contract on the front end or a signed contingency between you and your contractor, insurance companies like to depreciate the roof.

The depreciation is based on the age of the roof. So, for example, if your roof is 10 years old it’ll be depreciated by that much based upon what type of shingle you have.

We also get a lot of questions about the replacement cost value and the depreciation. Customers will often ask “Are you going to get your depreciation back?”

If you jump down to line number eight it says total recoverable depreciation and that number is the same as line number four which is depreciation. So that money is being taken out on the front end you can get it back at the end of the job.

Line Number 4: This is the calculated depreciation of your roof.

Line Number 5: This is the actual cash value. Cash value is the replacement cost value

minus the depreciation.

Line Number Six: This is your deductible and your deductible is something that you agreed to pay should a claim or should a loss happen. Some people have higher deductibles while some people have low deductibles, but this is what you are legally required to pay.

Line Number Seven: This is the net claim. In this case that net claim is what the first check from the insurance company was to the homeowner to get the work started.

Line Number Eight and Nine: The line items eight and nine are items that you can collect after the work is done. Once the work is completed, we draft up what’s called a COC or a Certificate of Completion and we will send our invoice and a certificate of completion to the insurance company with line items numbers eight and nine on our invoice. You will receive the depreciation back after we certify that the work has been done and it’s okay to release that depreciation.

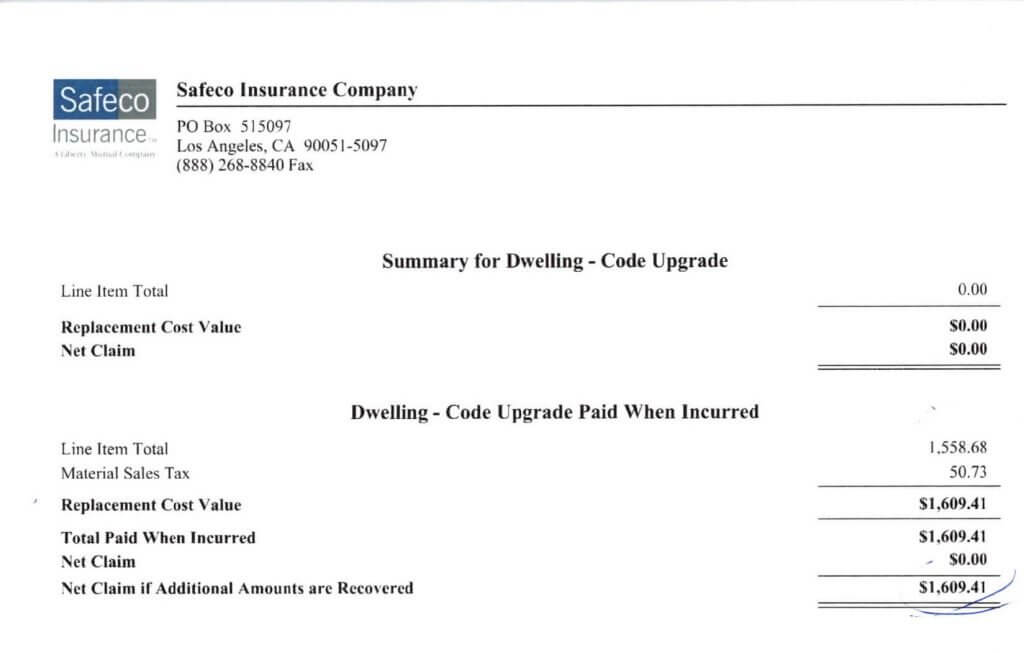

The second page in the insurance summary is the code upgrades page. In certain municipalities as well in insurance companies, if it’s required in your policy that you have code upgrade coverage then insurance companies will pay for that as well. In the Memphis area common upgrades are adding drip edge to the eaves and rakes of the house, adding ice and water shield in the valleys, and sometimes upgrading the decking if you have a lot of spaces. These items will bring your roof up to code.

We hope this outline will clarify the common questions we receive from customers on their home insurance claims. At Restoration Roofing we pride ourselves on being well versed with the insurance claims side of roof restoration.

If you suspect that your roof has damage, please give us a call at 901-854-3402 for a free inspection. We are your high quality, fair pricing roofer for the Memphis area here to serve you.